Share

Share  Download

Download  Posted on 10 Jan 2020 by Steve Johnson

Posted on 10 Jan 2020 by Steve JohnsonI had an early morning coffee with my grandmother on New Year’s Eve. Born in the 1920s and known to all my friends as Oma, she’s now living through the twenties again.

Asked what she thought of it, her only opinion on the matter was that “getting old sucks”. “It’s going to fly by, Steven. Make the most of it.”

Fly by it does. As we roll into the twenties of this century, Forager is entering its second decade. Founded in 2009, our Australian Fund turned ten during the December quarter (the Forager International Shares Fund launched three years later).

Reflections on the first decade

It’s been a good period to be invested in the stock market. The average annual return from owning the Australian All Ordinaries Accumulation Index was 8%, slightly lower than the long-term average of 11%. Globally, the MSCI All Country World Index returned 9% p.a. and the S&P 500, a broad measure of stocks in the US, 13% p.a.

Just being invested was the most important aspect to any investor’s returns in the teens. It was, too, the most important aspect to an investor’s returns in almost every decade of the past century.

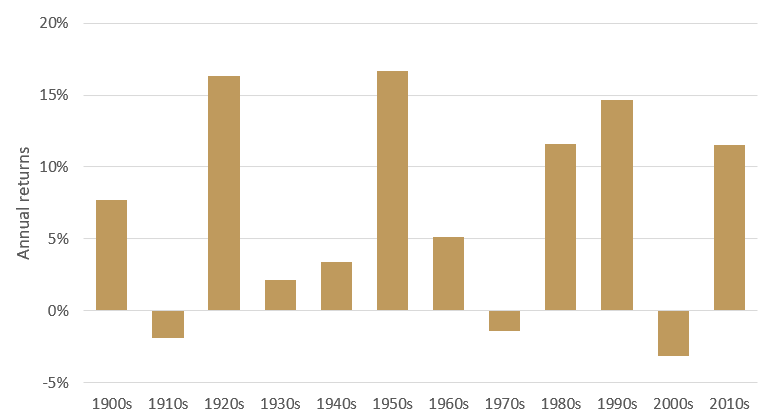

US Stock Market Real Returns by Decade

Source: Robert J. Shiller

There have only been three 10-year periods in the past 120 years where the real return (adjusted for inflation) from owning US stocks was negative. The worst of those was the naughties (2000-2009), where the real return was -3% per annum. I’m using data from the US market here because we have a longer time series but the returns from the Australian market have been similar.

Today’s zero interest rates mean a bank deposit is almost certain to lose roughly 2% per annum in real terms over the coming decade. For shares, the worst decade on record delivered only slightly worse than that.

Whether you invest with Forager, another fund manager, in an index fund or do it yourself, just being invested is the most important thing you can do. Don’t forget it.

Our job is to do better than that, and on that front there is plenty more to take from Forager’s first decade.

Learning on the job

It has been a steep learning curve. In 2010 Greg Hoffman and I ran for the board of mortgage company RHG. The company was amassing a huge cash pile as its mortgage book shrank and we wanted the board, chaired by RHG’s largest shareholder John Kinghorn, to pay it out to shareholders.

We didn’t win that battle with the Kinghorn family but the war was very successful. RHG was one of our most successful investments (and personally my biggest by some margin).

In 2012 we used the Takeovers Panel for the first time. RCU, a property trust we owned a large stake in, was gifting control to its largest shareholder through a friendly rights issue. We complained to the Takeovers Panel and successfully forced a restructure of the deal, invaluable experience that ended up preserving a lot of value for unitholders. Later that same year we ended up in the Supreme Court of NSW forcing the trust to give us our money back.

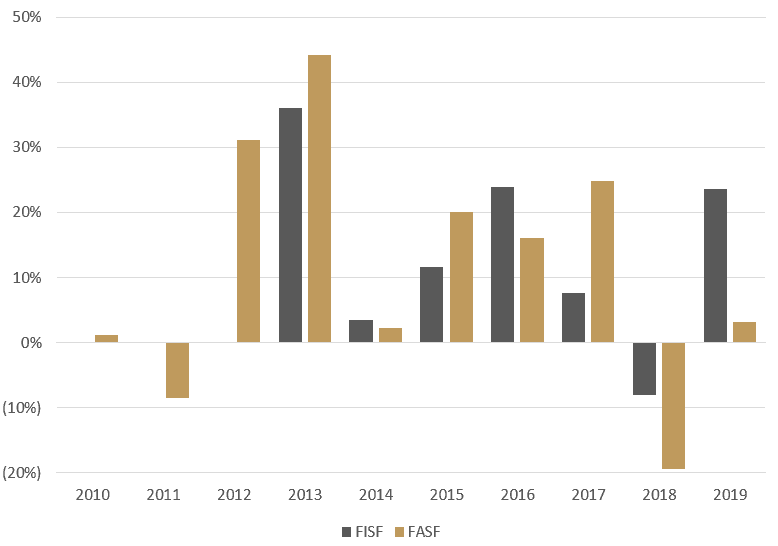

At this point we were still just three people: myself, Matt Ryan and Kate Ferguson. After a rocky couple of years (the Australian Fund was 10% underwater after the first two years), we started kicking some goals. As investments in distressed property trusts like Ingenia and Mirvac Industrial Trust paid off, investor patience was rewarded. The return for the 2013 calendar year was a whopping 44%. From the start of 2012 to the end of 2017 we launched a new International Fund and strung together six years of strong absolute and relative performance. Service Stream, Jumbo Interactive, Vision Eye Institute and Hansen Technologies were among the other big winners, more than offsetting the odd dud investment in the likes of Hughes Drilling and Brierty.

FISF and FASF – Performance by Calendar Year

That December of 2017 was the end of the good run, though, and we bookended the decade with another two-year period of even worse performance. The Australian Fund has lost 17% over the past two years, and the performance of the traded units has been worse.

Preparing for success

As you will see in our upcoming quarterly report, we’ve been making steady progress on resurrecting that fund’s performance. Periods of underperformance are part of the territory when running concentrated portfolios of stocks. Four years out of 10 years of underperformance is not far from what I would expect. But some things will be different in our second decade.

The biggest one for me is making sure we have the right people and business structure to succeed.

We have historically been good at making tough but important strategic decisions, the most significant of which was listing the Australian Fund on the stock exchange. We didn’t know when, but we knew that fund was going to suffer periods of underperformance, potentially significant. Not having the pressure of outflows over the past few years has been fundamental to the long-term prosperity of the fund.

But there are things I would do differently. In early 2013 we launched an International Fund with two new analysts and a lot of the same clients. Then we lost a few key staff members, including both Matt and Kate heading off to do something different with their lives. Trying to manage a new fund, a new team and find replacements for people who were instrumental in our success put significant organisational strain on the business.

Late last year I listened to a great interview with Daniel Ek, the founder of Spotify, on the Invest Like the Best podcast. Talking about his early management lessons, Ek explained how a Dubai chocolate maker taught him that a growing business needs to “build in a buffer” if it wants to be successful. While growth is great, it also creates problems that will need to be fixed and resourced.

We’re not trying to dominate the global market for audio like Spotify, but the same is true for any business. If you don’t invest in anticipation of growth, then the growth you are hoping for can be the thing that brings you unstuck.

I don’t for a moment regret launching the International Fund. Its returns have been healthy and the experience gained so far is going to be invaluable. I want it in my own portfolio and think it has a very important role to play in yours. We just need to do a better job of preparing for success.

The past two years have seen a lot of investment in human and financial resources, at both a board level and in the investment management teams. As a business we head into the twenties much better prepared to deal with unexpected hurdles and, hopefully, growth.

http://https://www.youtube.com/watch?v=iTegrLmFzK8

Flexibility

I’d also like to see us more flexible with construction of our portfolios.

That means being contrarian when contrarian ideas are offering attractive payoffs, but willing to keep it simple when those great opportunities don’t exist.

We owned some high-quality businesses in the early days of the Forager Australian Shares Fund. Businesses like Macquarie Airports (subsequently slimmed down and renamed Sydney Airport), Spark Infrastructure and ARB Corporation.

You should prepare for us to own them again. Consistency is something every financial advisor wants from their fund manager. I want you to prepare for inconsistency.

Over the next decade, I want us to do a better job of adjusting portfolios for whatever market environment we are presented with. The big returns are still going to come from small, unloved and contrarian ideas. But there’s nothing wrong with higher quality, reasonably priced investments while we wait for those ideas to present themselves.

Less cash, more shares

And finally, I want our funds to hold less cash.

You need to be invested. And so do we. We’ve made mistakes over the past decade. We’ve written mea culpas. But the most significant negative impact on performance was holding too much cash for long periods of time. A deeper investment team and a stable of larger, quality companies will help. But I will be more vigilant about being mostly invested, most of the time.

The fun part

For all of the stress of the past two years, I’m immensely proud of what we have built over the past decade. We’ve survived, grown and made a lot of money for our clients.

An investment of $100,000 in the Australian Fund at inception is worth $264,115 today* and $100,000 in the International Fund has turned into $238,124 in less than seven years.

Yes, it’s been a friendly backdrop. Yes, I’m hopefully writing to you in a decade saying we have done better. But, from a one-man shop 10 years ago to a team investing money all over the world, we have come a long way. The experience should serve us well.

The next decade will also fly by. Who knows, my Oma might even see it out. Come what may, I promised her I will enjoy it. But making you some great returns is going to make it all the more pleasurable.

* Returns calculated at 31 December 2019 using NTA, not market price. At the last traded price on 31 December, the value would be $229,141.

This is an excerpt from the upcoming December Quarterly Report – if you would like to receive this report (and all future reports) in your inbox, you can register to do so here.

Thanks Steve and growing II team.

You did prepare us for periodic underperformance.

I’m unconcerned and actually quite pleased to see them.

I almost bought some more stock – FOR being down 15% from NTA – but have set an arbitrary 20% – as I am ‘overweight’ FOR.

Thanks for the journey and the education.

PS; Your RHG advice was transformational for us too as it allowed us to buy a city townhouse from which our kids were based to attend city unis.

I have been an investor since the beginning and opposed the listing of the fund on the sharemarket. I have lost confidence. This update reinforces my suspicions that “spin” has overtaken substance. It was not that long ago that my investment in the Australia Fund was worth more than $200k. Now it’s $138k and all this taking place during a period of record share prices. I am sorry to say that I can find nothing positive at all in this. There is little to be proud of in the recent past and no amount of glossing over the awful performance since listing can change that.

Hi Greg, I disagree with your premise. Welcome to long term investing. Josh

Hi Greg,

Thanks for the feedback. I completely understand the frustration and am a significant investor in the fund myself.

Firstly, on the communications, we’ve been very open and transparent about the stuff-ups over the past 18 months. It’s time to move on. The fund’s performance has been better the past 6 months and we know full well that we need many more years of that – but wallowing in the mistakes of 2018 isn’t going to help.

On listing and the traded price, I am only more convinced that it was the right move. There are clearly investors unhappy and frustrated, like yourself, and willing to sell at a discount. Under the old open-ended fund structure, that could have been a terminal risk. Funding redemptions by selling stocks with the current liquidity in our holdings would have been a very painful exercise. So yes, it is bad for those who want to sell. But for the majority of investors in this fund who want to hold it for the long-term, they have been protected from that risk.

We know we need to perform. Unlike most LICs, there is no long-term management management agreement or poison pill protecting us. We’ve made a step in the right direction recently and plan on adding to it over the coming years.

Kind regards,

Steve

steve, ‘fortune favours the bold’ with holding less cash and lumpy returns and under performance with inconsistency for 2-3 years in 10yrs…

as Steve J says – ‘in search for extreme dislocations…’

admin ✅✅✅ lead and be serving of Forager analysts

most of all, maintain team cohesion at all costs…

Forager inconsistency is purposeful consistency over a very very long term of investing

this best sums up Forager thinking:

“The fellow that can only see a week ahead is always the popular fellow, for he is looking with the crowd. But the one that can see years ahead, he has a telescope but he can’t make anybody believe that he has it.”

The only decision I was unsure about was when you sold all your shares in Service Stream and Jumbo Interactive, I thought you may keep a smaller position.

It’s easy to be an expert now, but you had something very valuable in the stock market (a low entry price), so even small increases in earnings can give good portfolio performance. Of course, I appreciate that any profit downgrade will also hit you harder, but I didn’t see these stocks as being particularly overvalued or high risk.

Greg, yes, since listing in December 2016, it has been a most disappointing ASX market price trading at 15% premium to NTA, down now to 15% discount to NTA… coupled with the gains of calendar 2017 all but lost in calendar 2018

In Building the Ark whilst the Sun is shining…

https://foragerfunds.com/news/fixing-future-forager-australian-shares-fund/

and we parents, as founding 2010 members encouraged our sons with a combined SMSF, with a FOR investment in July 2017 with prices at $2, and rights offer in Sept 2018 $1.58…

that said the investment is for multiple decades to come…

for all of us, it is the very long time in the market…

as an aside, there have been many unlisted open managed funds that have folded in recent times due to demand on redemptions…

finally, for the contrarian investors with a telescopic very long view of investment, this is an optimum time to be buying FOR at 15% discount to NTA at $1.15 to be the vanguard position.

I would be interested in hearing Steve’s view of how he thinks the asx listing has gone. One of the things I think my wife and I never considered was that the fund would trade this far below NTA. As I understand it (now), there are funds that have traded at approximately 15 percent below NTA for, well, decades.

Anyway, you have to take the good with the bad. Thanks for the last 10 years guys.

We invested with our eyes wide open. We knew that there would be lumpy returns. We don’t have any complaints as we own every decision.

Man, I’m so sick of seeing fund managers debate cash levels. You’re paid to beat the market. Whether you do it with 5% or 30% cash levels is irrelevant.

I hope the flip side to paying up for quality is that you reconsider the idea that a morally dubious business is a great investment at a cheap enough price. Hindsight is always 20/20, but some of your biggest loses, even before starting the fund are companies that you would never ever personally use or associate with. Maybe there is something in that.

Lumpy returns are one thing. No returns quite another – even worse if you reinvested your dividends which we have. We are in loss on every single ASF purchase since our first on 22nd February 2013, at $1.239, to our last at $1.615.

In July 2018.

7 years of negative returns in a market at record highs.

Hi Michelle,

It’s been a rough 24 months but the past 7 years have seen decent returns from the fund. Nicole has sent you an email setting out your returns over that period. Get in touch if it doesn’t make sense but it is very important to include your distributions as a component of the total return. As a trust we will pay out all income (including capital gains) over time. So most of your return is going to accrue as additional units (assuming you reinvest), rather than accretion in the unit price. Over the past 7 years, distributions have totalled more than 80c per unit.

I tend to agree with the negative sentiment here too and object to the spin that if you’d invested 100 K at the start it would be worth 264 K. Unfortunately, I did not, as I did not have the means then to do so back then. My returns are just over 3% across two accounts, including distributions, over my holding period of several years.