Share

Share  Download

Download  Posted on 16 Sep 2015 by Steve Johnson

Posted on 16 Sep 2015 by Steve JohnsonThere were a few surprises for me when reviewing Blackmores’ (ASX:BKL) recent results for yesterday’s mea culpa. I was surprised how much of the revenue growth was in Australia. I’m not sure why, but I had the idea in my head that it was Asian demand driving the company’s stellar share price gains.

Asian sales were up 26% last year. Impressive, sure, but nothing on the 43% growth in Blackmores’ home market of Australia.

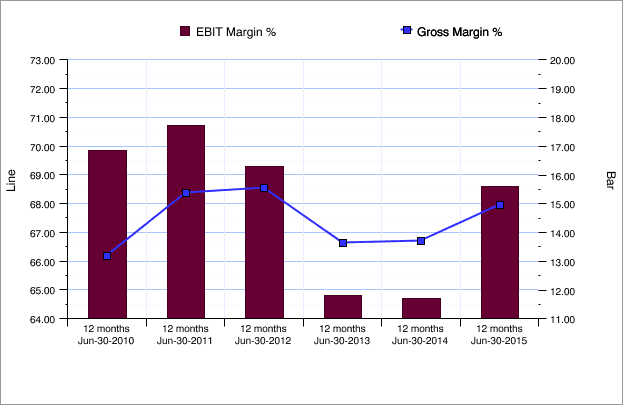

Even those growth rates aren’t enough to justify a 300% increase in the share price, though. The other crucial factor is that margins have rebounded to the levels of a few years ago, driving a dramatic increase in profit. It seems Blackmores has regained some pricing power.

That seems true even anecdotally. You still see Swisse and Nature’s Own on television, but Swisse in particular is not as prominent as it was. So what’s going on?

This morning’s AFR suggests Swisse is about to be sold to Chinese private equity firm Hony Capital. If Swisse has been dressing itself up for sale, it would make perfect sense to take the foot off the marketing accelerator to improve margins and make the company seem as profitable as possible.

We’ll soon find out whether Swisse’s new owners are happy with the status quo. Blackmores shareholders will be hoping so.

Whist true the 43% headline Australian growth figure, it actually masks an enormous amount of product that is getting shipped to China thru’ Australian channels. Pharmacists & other distributors constantly get approached by Chinese nationals wanting to place $50,000-$100,000 orders of stock at “cost plus 2%” for shipping to China. They’d love to do it as apparently the orders would be continuous; problem is Blackmores can’t supply stock as many of their retail end suppliers are clamouring for the same thing and their plants are working at capacity. Blackmores are rationing stock as a result to their retail accounts would you believe.

VERY interesting comment Stephen. Wow.

Its likely that many international buyers of the product are also manic buyers of the shares as seems to occur in Bellamys and Capilano Honey. They care nothing for PE ratios – just brand name, country of origin, and the resulting perceived quality.

Back in ’09 I had an at limit buy order for BKL for just a couple of cents below what would eventually turn out to be the trough (a little over $12). I never chased the stock and indeed completely missed the boat on that one.

It was reminiscent of the anecdote that Phil Fisher relates in “Common Stocks”.

You need to pay more attention to the Chinese community in Australia. There is very little trust of large importers in China, so products imported by individuals with family connections in Australia sell for a premium. Milk powder is the big one, but for anything health related trust is a big part of the purchasing decision. The perception is that Australia gets the real stuff, and people that send it over mark the packaging to be reasonably sure it hasn’t been tampered with. The actual brands chosen seem somewhat irrational, based on word of mouth reputation in China, but if you pay attention to what people are starting to send you will know which products will be consistently selling out in the coming months. There are Chinese language stores that do the shipping close to many shopping centers, though importantly, the senders box the items themselves.