Share

Share  Download

Download  Posted on 25 Jun 2020 by Gareth Brown

Posted on 25 Jun 2020 by Gareth BrownAn investor recently wrote asking whether we’ve looked at the world-changing opportunities in the software as a service (SaaS) sector. With a reputation for buying beaten-down value stocks, it might surprise some of you just how important technology is to our International Fund. This post is to clear any misconception.

SaaS, sometimes referred to as on-demand software, is a fancy acronym for subscription-based software delivered online. In days gone by, customers bought perpetual licences and stored the software on their hard drive. These products lasted as long as it was useful (in the world of software, that’s typically years not decades).

Customers today pay a monthly or annual subscription, with ever-updated software accessed externally as needed rather than stored on your local device. SaaS products are always up to date.

Stocks with a SaaS story have massively outperformed the wider market over the past decade. Partly that’s because, as Marc Andreessen noted nearly a decade ago, software is eating the world. Software is becoming more and more important to our lives, and a larger and larger part of global economies and stockmarkets.

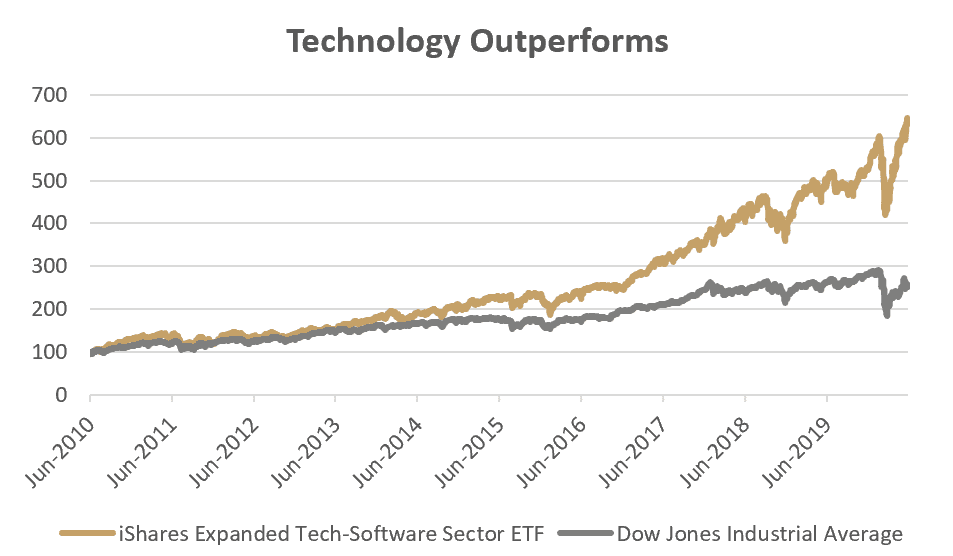

The chart below shows how much a basket of technology/software stocks has outperformed the (decidedly lower tech) Dow Jones Industrial Average over the past decade.

Source: Bloomberg

The subscription model has proven very lucrative for software companies versus their prior business models. The benefits, from the businesses perspective, include higher average annual prices paid by users, higher renewal rates, no chasing up users to buy updates, lower advertising costs, no physical production or packaging and less revenue sharing with retailers and sales partners.

Hyped sector

There’s also, arguably, over-excitment in the sector at present. Most of the outperformance of software stocks happened in the back half of the decade.

In contrast, 2010-15 was actually when most big software companies started the shift towards a SaaS model. That meant giving up chunky revenue from selling perpetual licences in order to switch customers over to paying an annuity stream. A significant creator of value for software companies in the long run, it suppressed revenues and profitability over the multi-year transition period.

The market took a few years to price this correctly. It now largely does so. But if anybody is extrapolating growth from the past 10 years into the next 10, they’re partly extrapolating a business model shift that won’t happen a second time.

So, there’s a lot to like about entrenched SaaS businesses, and we have no argument with the idea that the world is changing rapidly. The trick is to find opportunities where the hype isn’t reflected in the stock price. That usually means searching tangentially to the main SaaS narrative.

Geographic orphan

GAN (Nasdaq:GAN) is hopefully illustrative, it’s been one of the Fund’s most successful investments lately. When we first bought the stock toward the beginning of 2020, it was already on the path to being a very important provider of business to business (B2B) software systems for casinos and sportsbook operators in the fledgling US online gambling market. Listed in the UK, on the secondary AIM market to boot, it was a geographic orphan.

Many Americans interested in the sector claimed they couldn’t buy GAN until it relisted in the US. As silly as that sounds, upon moving to the Nasdaq recently the stock shot up like a rocket. We’ve been slowly taking profits since.

Autodesk (Nasdaq:ADSK) is the leading computer aided design (CAD) software for architects and the building industry globally. It’s a more conventional SaaS story. But it’s been another big winner for the Fund. Past midway through the conversion of licences from upfront to subscription, and with recession fears likely weighing on investors’ minds, the market had the stock wrong when we bought most of our position during the panic earlier this year.

Blancco (AIM:BLTG), once again the Fund’s largest position, is an investment well-known to most unitholders. Whether it’s classified as a SaaS stock is irrelevant. It has very high retention rates among customers, who regularly return to buy usage licences typically based on volume, and mostly take delivery of the software remotely. Sound familiar?

SaaS-like

Then there are stocks like Auto Trader (LSE:AUTO) and Spotify (NYSE:SPOT), technology-led and with customers paying by the month. And Uber Technologies (NYSE UBER) is a tech intermediary with revenues linked to customer usage. The Fund has done very well out of all of them.

More recently, we’ve bought into a business providing data-driven services to the auto financing industry. There will be more to say in a future quarterly report.

This is not a fund that avoids technology or growth opportunities, they make up an important part of the portfolio. We fully recognise there’s significant and growing value in large pockets of the software and broader tech industries. As always, however, mispricing is a prerequisite. Here’s hoping for similar opportunities in future.