Share

Share  Download

Download  Posted on 23 Feb 2016 by Gareth Brown

Posted on 23 Feb 2016 by Gareth BrownAccounting and reporting to shareholders is a soft science at best. That annual report you’re reading isn’t the absolute truth. It’s an interpretation, a tainted one. The best you can hope for is it’s not too tainted.

It is the sort of thing analysts are reminded of every day. But few examples are as stark as UK giant Rolls Royce. The company makes power systems, most importantly engines for wide-body jet aircraft. We own Rolls Royce in the Forager International Shares Fund. We like the opportunity. We suspect the investment will do well and went in with eyes wide open to the issues about to be discussed..

But, as you’ll see, the accounts are tainted. Here are just a few of the instances where Rolls Royce’s reporting diverges markedly from how a rational shareholder might want things reported to them.

Mythical order book

The first digression occurs before the company even makes a sale. Rolls recently reported an order book of £76bn at 31 December 2015. That’s a book of future sales that stretches out for a decade. More than 85% of that order book relates to the civil aerospace business—engines for commercial aeroplanes—and includes both new engine sales and up to seven years’ worth of long term maintenance contracts.

Surely the company will make new additions to the order book in the coming years. And some of those maintenance contracts, which only include seven years of work in the order book, will run for decades. You might think it safe to assume, as a useful starting point though, that £76bn worth of contracted engines, parts and services in the order book will generate £76bn of sales over, say, the next decade.

Nope.

The issue is that the order book is put together based on the ‘list price’ of the engines that have been ordered. The list price is a largely mythical construct. Well, it might apply if an airline ordered a single engine, for delivery next week, to the Gobi Desert. But otherwise, buyers always get a discount. You won’t find the scope of those discounts anywhere in the annual report. But they’re massive—quite a bit more than 50% on forward orders of whole engines, and perhaps 10-20% on aftermarket parts. Of that claimed £76bn order book, we’d guess at least £30bn will never flow through as revenue to the company. Thirty billion pounds!

Any analyst worth their salt can work this out and work around it. It gets more complex when we move on to the accounting for actual sales.

Mythical profits

In the recent Forager Funds December 2015 quarterly letter, we describe Rolls’ engine business as being a version of the ‘Gillette model’. Gillette is happy to sell razor systems for no profit, because it makes so much profit on the blades it will subsequently sell you.

Somewhat similarly, Rolls Royce sells its aircraft engines at an underlying economic loss, typically in the vicinity of 10% of purchase price. But, over the life of that engine, the company makes 3-4 times as much revenue from parts and service, typically at underlying economic profit margins of 25% or more.

Note I said underlying economic profit/loss. Because what goes through the actual profit and loss account is very different indeed.

Imagine an illustrative but realistic sale of engines that generate £100m of revenue on delivery of the engines, with a 10-year parts and service contract signed to maintain those engines that generates £15m of aftermarket revenues annually. So the company can expect to generate £250m in total sales from the contract, £100m in original equipment sales and £150m in aftermarket parts and service revenues over the subsequent decade.

Chart 1 below highlights the earnings before interest and tax (EBIT) on that mythical contract based on various accounting standards.

The blue line, titled ‘Underlying’, highlights how the company would report this deal if I owned Rolls Royce outright, and fairly closely matches the company’s real cash flow position. The company loses about £10m on the original sale (a 10% loss), but makes 25% profit margins in the subsequent aftermarket revenues to follow.

In stark contrast, the orange line describes how Rolls Royce actually accounts for profit when the engine and aftermarket contract are signed at the same time, called ‘linked’ accounting. Instead of ‘losing’ 10% on the sale price and gaining 25% on aftermarket revenues, they work out a blended margin (11% in this case, it turns out) and apply it to all revenues as they are received.

Thus, a loss of £10m on the original sale becomes a profit of £11m. Not bad huh. Except that profit won’t represent real cash coming in the door, and they’ll need to fund the difference. Note the profit over the whole life of contract is the same, at £27.5m, But they’ve completely ‘front ended’ the profit of the contract, over-reporting on the initial sale and under-reporting an offsetting amount of profit on service revenues over the rest of the decade. It’s a neat accounting trick.

It’s important to point out that this example is not perfectly accurate, the accounts actually shift a little revenue around too. But the point is simplified and roughly right.

The grey example highlights how the company records profit when the original sale and aftermarket contracts are signed separately and independently, and thus cannot be linked because accounting standards won’t allow (usually separate contracts with the airframe manufacturer, Airbus or Boeing, and a separate maintenance contract with the ultimate aircraft owner, usually an airline or lessor). These are called unlinked sales. In this case, they don’t report a profit on original sale but they do ‘capitalise’ the loss, and amortise it (feed it through the profit and loss statement as an expense) over the subsequent life of the maintenance contract. The accounting treatment isn’t as aggressive as linked sales, but it’s still head in the sand stuff.

Complexity

Not only do we currently have the company aggressively bringing forward profits but, because of changes to the nature of the industry, the business is shifting from predominately linked sales to predominately unlinked sales. Whereas the business was 80% linked a few short years ago, it will be 80% unlinked a few more years from today.

This shifting mix is creating massive complexity. While the above example of one contract is easy enough to understand, piecing it together on a whole-company basis is torture. Rolls is now reporting new sales with less aggressive accounting treatment, some older (linked) sales that massively over-report genuine economic profit, older (linked) maintenance contracts that underreport economic profit and cash flow, and newer (unlinked) maintenance contracts that are somewhat closer to economic reality but still skewed.

As Charlie Munger is fond of saying, when you mix raisins and turds, you get turds.

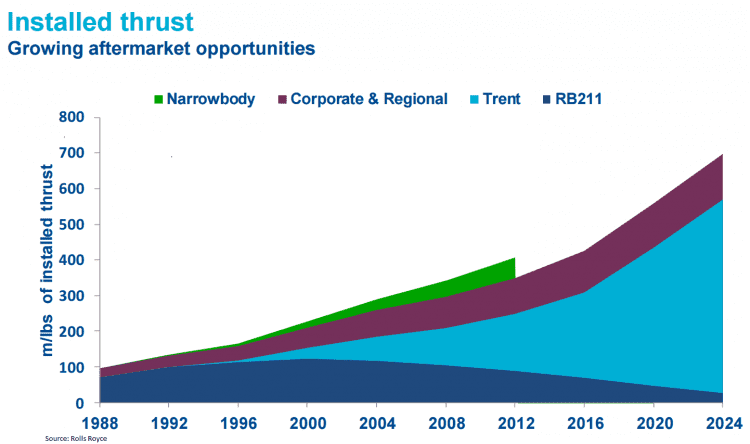

And so analysts look into their bag of tricks for workarounds. Here’s one of the simpler ones. You focus purely on the Aftermarket business—parts and service—that is the real goldmine of this operation. If we can understand that profitability well, and make some deductions for expected losses on original equipment sales, we’ll be 90% there.

The chart below, which is published in every Rolls Royce result, thus becomes a useful analytical tool. It highlights how many million pounds of thrust there are in the installed base of engines on service contracts with Rolls Royce. The installed base is a very good guide to future maintenance revenue growth. And as you can see, a chief part of the bull case for the stock, it’s destined to grow very rapidly over the next decade. That’s great. Work out what is the fair underlying economic profit on today’s installed base, amplify it for the coming growth, make some necessary deductions. Margarita time.

Oh come on, surely you know by now that it’s never that easy.

While Rolls Royce tends to legally own 100% of each engine program, the economic reality is, once again, a bit different.

A significant proportion of the materials and labour that goes into each engine and each spare part comes from outsourced partners—typically more than 75%. And, while some of those suppliers do it for standard pay as you go rewards, more crucial partners often have a financial stake in the engine program via a so-called risk and revenue sharing model. So if a new engine model goes well, some partners share the spoils. If it flops, they share the pain. It’s good risk management on Rolls Royce’s part.

And the percentage of ownership that effectively belongs to partners on the new model engines, at around 35-40%, is much higher than on the older models. Again, you won’t find those numbers handily in print in the annual report. But they’re crucial to understand.

They’re important because chart 2 above, and the numbers that underlie it, are based on gross thrust, not Roll Royce’s net share. And so that chart overstates the coming growth from Rolls’ shareholders’ perspective. Don’t adjust for it and our simple workaround, designed to cut through the complex accounting, falls flat.

I’ve talked with several very numerate Rolls Royce shareholders that had missed that point.

So there you have it – a company with a wide and deep moat and, finally, decent management. Its accounting is, like its engines, firmly in the clouds. The bears are underestimating it and some bulls are surely overestimating it. We own the stock, but will do so with a healthy level of scepticism in any business where the accounting is this opaque.

Made me think of Buffett’s four questions to auditors:

1. If the auditor were solely responsible for preparation of the company’s financial statements, would they have in any way been prepared differently from the manner selected by management?

2. If the auditor were an investor, would he have received – in plain English – the information essential to his understanding the company’s financial performance during the reporting period?

3. Is the company following the same internal audit procedure that would be followed if the auditor himself were CEO? If not, what are the differences and why?

4. Is the auditor aware of any actions – either accounting or operational – that have had the purpose and effect of moving revenues or expenses from one reporting period to another?

Back in 2009 or 2010, I took a good look at Penrice Soda Holdings, because it was, prima facie, ridiculously cheap, at something like 4 times reported earnings.

They were in the business of producing soda ash from a vertically integrated mine and processing facility, and in the course of digging this stuff out of the ground they were, like every miner, creating a huge amount of crushed rock as a byproduct of their mine.

Not only were these crooks recognising the crushed rock as inventory (with any additions to their crushed rock pile duly being recorded as on the grounds that they MIGHT be able to sell it IF the city of Adelaide expanded in their direction in the near future), but they also recognised the resultant hole in the ground as a landfill site under construction, again with changes in the “value” of their landfill going through the P&L as revenue! Incredibly, a Big four accounting firm signed off on their accounts.

My M.O. is to first buy a stock when it is prima facie cheap, and to then do the serious digging through the accounts while I hold a small position. I find that having skin in the game when I’m looking at a stock incentivises me to really get my head around things more so than if you’re looking at the accounts from the sidelines.

When I read the note that explained what they were doing with their rocks and their hole in the ground, I first didn’t believe what I’d read and thought that I must have misunderstood something. When a re-reading of the annual reports confirmed my earlier view, I sold my position (with a dumb luck profit to boot) in what must have been one of my fastest ever sell orders.

I am still amazed that they managed to last another three years before going bust.

Don’t be shy SG, which Big Four Accounting firm signed off on the accounts, and the name of the auditor.

The lack of personal accountability of professionals is a big reason why these things are spoken of in such a cynical way., and why they get away with it.

I’m always amused by the way one of the main accounting professional organisations (CPA Australia) is more concerned with promoting its CEO (Alex Malley) and his constant harping on about leadership, than dealing with the real accounting issues of the day such as revealed by some of the Forager articles. Perhaps CPA stands for Centre for Promoting Alex or as one AFR commentator suggested Charming Prince Alex.

I suggest the CPA board needs to rethink whether they are serious about accounting issues or if they exist to promote you know who.

It’s an indictment of the accounting profession, and perhaps this accounting professional organisation, that I learn more about the financial shenanigans of corporate reporting from the Forager staff than from them.

Here’s the annual report that I looked at: http://www.asx.com.au/asxpdf/20100923/pdf/31sp24ffm7bh1n.pdf

I think that there is a lot to be said for going over the old annual reports of busted companies.

In fairness to the auditor in this instance, I think that Penrice soda did indeed actually sell of its crushed rock as aggregates to paying customers, but it was a relatively small portion of the total amount of rock that was extracted, so their inventory figure kept on rising year after year, and with all that extra ‘revenue’ that was being recognised, they maintained ‘healthy’ reported profits, even though they were continually, and massively FCF negative.

The auditor of Penrice Soda Holdings Limited for the 2009 (and presumably the 2008 ones also) Annual Accounts was Colin Dunsford of Ernst and Young. He was a managing Partner at Ernst and Young having come from Arthur Anderson in 2002. He retired from E & Y in 2010.

The auditor in 2010, 2011, 2012, 2013 was Mark Phelps from Ernst and Young who is now Head of E & Y’s audit practice in Adelaide. Also came from Arthur Anderson in 2002.

Penrice Soda Holdings Limited was placed in liquidation in August 2014

Pingback: Pliable Accounting Leads us all Astray - Forager Funds

Very interesting commentary in relation to Penrice Soda auditing from the EY “Assurance” group. Mark Phelps (EY auditor responsible) is personally aware of investor concerns in relation to this expressed in this forum. It will be interesting to see if he has the wit and courage to fully explain his actions.

A quick review of the Auditors Remuneration per the Penrice Soda annual reports from 2008 through to 2013.

1. 2008 – $235,361; 2009 – $369,687; 2010 – $349,188; 2011 – $397,954; 2012 – $334,973; 2013 – $306,229

2. Non-audit fees were more than 50% of the audit fees in all years except 2013 when they were just 30%. In 2011 they were more than 85% of audit fees. I mention this not because this is different to many other public companies (which it isn’t) but because of the danger of auditors generating fees from clients other than from audit work. A danger that CLERP 9 endeavoured to counter but it seems to be a growing problem as auditing can be seen as a foot in the door to clients for the more lucrative consulting type work. Think Enron and you should be able to visualise the dangers of this. Not too sure what the non-audit fees comprised with Penrice Soda but I would have thought above 55% of audit fees is worth asking the question.

3. Not very good proofreading of the annual report because on the relevant notes on Auditors Remuneration the figures are shown as millions not thousands. No big deal as pretty obvious but for any pedants here are the references. note 26 page 77 of 2009 a/r, note 26 page 88 of 2011 a/r, note 25 page 79 of 2013 a/r

Very illuminating Brett.

It is interesting the response received from Mark Phelps, the responsible auditor from the Adelaide office of EY. Somewhat predictably Mark Phelps behaved like a complete wimp when confronted with this Penrice issue. Here is his response:

“EY is not able to comment on matters regarding our former or current clients. If you have queries in relation to Penrice Soda Holdings Limited, please refer these to the company administrators.

Kind regards

Mark ”

Possibly we will get at some stage an EY “company response”, however I would not hold your breath.

Pingback: Rolls Royce Cleared for Take Off - Forager Funds