Share

Share  Download

Download

Flash back to April 2007 and Orica investors could be forgiven for asking what could possibly go wrong? The board had just rejected a takeover bid at a substantial premium to the prevailing share price, which was already up sixfold in the previous six years. This was (and still is) a company whose core explosives business benefits from being in a global duopoly with significant barriers to entry and was generating returns on equity around the 20% mark.

Fast forward to May this year and yet another disappointing half-year result. The share price has declined 58%, return on equity (pre write downs) has roughly halved and profits have declined.

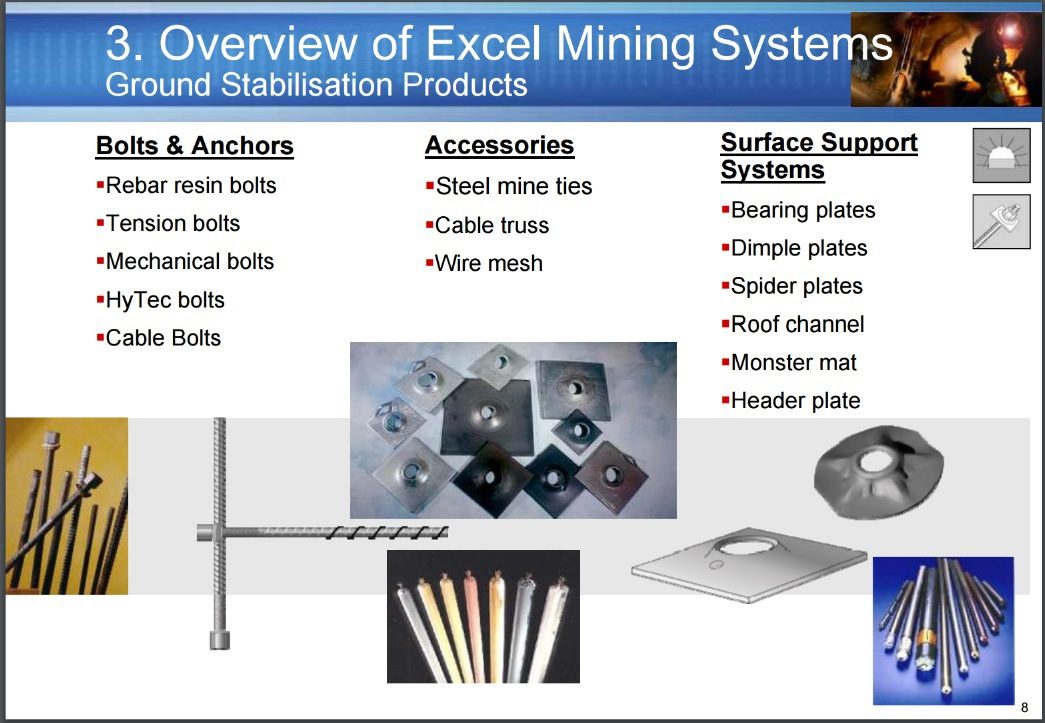

So what went wrong? Around the time the board rejected the takeover approach, the company made two major acquisitions to ‘diversify’ into the mining services sector. Minova (October 2006) and Excel (September 2007) were acquired for $857 million and $775 million respectively. Excel was consolidated into Minova and this new operating segment generated $150 million EBIT in 2008, more than 15% of Orica’s total EBIT. Yet this business lacked the competitive advantages of the core explosives business. Its primary exposure is to underground mining where producers are often high up the cost curve and making a profit is highly dependent on the coal price. Compounding this was significant exposure to volatile developing markets and a product range that didn’t appear to require much technical expertise. Indeed, one of its major products, steel roof bolts, looks like something a coal miner could acquire from their local Bunnings.

Following the end of the mining boom, Minova’s earnings evaporated, making a first time operating loss of $19 million in 2015.

The remainder of Orica’s business has been remarkably resilient since Minova was acquired. This is because its core explosives products are a key input into mining production but only a few percent of the cost of total production. In the grand scheme of things they are a small but essential cost to miners. Despite the end of the mining boom, miners keep producing, the world still needs coal and iron ore and commodity prices aren’t as big an issue for Orica as for other mining services companies. At least they weren’t, until Orica acquired Minova.

We all make mistakes.

Liquidate Minova and Excel.

What do we get back?

Back to our strengths.

FYI, roof bolts in an underground mine are designed to show miners how much the rock above has sagged/shifted since the bolt was installed, which can provide early warning for cave-ins.

Not the sort of thing that they sell at Bunnings.

Well……. yes SG. But the point that you seem to miss is that those roof bolts (and similar items) are available through many different mining services suppliers and do not have the ‘moat’ that the Orica explosives business has.