Share

Share  Download

Download

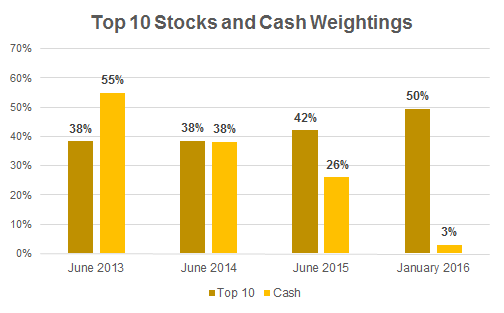

The Forager International Shares Fund’s cash balance has fallen to below 3% from about 13% at the end of December 2015, its lowest level since inception. This made me ponder the role of cash in a fund like ours.

Many investors like having some cash, or ‘dry powder’, in their portfolio to take advantage of opportunities that may suddenly arise. Market corrections occur unexpectedly and being fully invested can restrict investors’ ability to snap up assets at bargain prices. Some like to keep a minimum allocation to cash, say 10%, at all times.

To a value investor this makes perfect sense – you don’t want to be short of cash at a time when Mr Market is most likely to offer you the best deals. Yet this is one value investing credo I feel differently about. Let me explain.

We are not market timers but stock pickers. Clients pay us to find cheap stocks across the globe and I believe we should be invested 100% of the time in our good ideas. If a market correction comes and superior opportunities arise, we should be prepared to sell cheap stocks to buy even cheaper ones.

What if we don’t have enough good investment ideas? Should we go for our second best ones? I don’t think so. As Seth Klarman puts it “Where does it say that investing means always buying something, even the best of a bad lot?”.

What I am suggesting is that the Fund’s cash balance should reflect the level of attractiveness of the investment opportunities available to us at a given point in time. And not a prescriptive or target level cash weighting. And definitely not a minimum. If we have the ideas, we should be fully invested. If we don’t, we shouldn’t.

Since we launched the International Fund in February 2013 we have experienced a raging bull market. Low interest rates forced many investors to lower their required rates of return, pushing stock prices higher and higher. In this environment we didn’t find enough stocks that met our stricter investment criteria and so the cash balance remained high.

This month’s sharp decline in global stockmarkets has provided opportunities to deploy more cash. Two new companies have made it into the ‘top ten’ and we added to some existing investments. This resulted in the Fund’s cash balance falling to 3%.

Should we be selling some ideas we like just to get that cash weighting back up above 10%? Many, including some of my fellow Forager colleagues, think so.

You could argue that we have been able to take advantage of the recent sell off because we had that cash available, and that without that flexibility we won’t be able to take advantage of even better opportunities if they arise.

But we can always swap good ideas for better ones, especially given the International Shares Fund owns plenty of stocks with good liquidity. And it is my view that, provided that those best investment ideas are available, it is less desirable to hold cash at all times just because some opportunities might arise in the future.

I know this is a controversial stance – there is no doubt we will experience worse bear markets than this one – but I am more excited about today’s portfolio than concerned about the lack of ‘dry powder’. That is no guarantee that we will make money in the coming months. But I think that the current portfolio gives us a better chance to outperform in the long term than the old one did. And I also think it will beat one sitting on a huge pile of cash.

Forager Funds is very different to individuals and small businesses. It strikes me that most Funds probably keep cash to pay for redemptions. Forager Funds is young and your cohort of investors maybe robust, however, death, sickness, divorce etc will cause a natural turnover factor.

3% therefore sounds too little cash.

Still if there are more significant market falls either pass the hat around again or suspend redemptions.

Hi Craig, interesting point you raise about exiting the fund with a payout from cash. My view is the buy / sell spread should allow for any need to sell off securities to balance the real time difference between depositors and redeemers. This is fair to fund holders. The opportunity cost of cash not fully invested is difficult to quantify. A conservative focus on value by the fund manager is preferred, without trying to time the market. Investors can hold their own cash (to ride out a market melt down) or have a bank finance facility available when value abounds.

Look no further than industry super funds with low cash allocation able to outperform retail super funds that hold cash to cover potential redemptions. The industry fund with its default option advantage will receive guaranteed new deposits in line with the increase in employment.

Does the fund ever park cash into merger arbitrage situations in lieu of cash to eke out a few extra points ? eg Berkshire’s takeover of PCP springs to mind as an obvious almost riskless example

Not ‘in lieu of cash’ as such. But if a risk-arbitrage stacks up nicely as an outright investment, with adequate value and margin of safety, of course we’re always on the look out.

I like this Buffett quote : http://www.marketfolly.com/2010/09/warren-buffett-on-holding-cash-quote-of.html

“We always keep enough cash around so I feel very comfortable and don’t worry about sleeping at night. But it’s not because I like cash as an investment. Cash is a bad investment over time. But you always want to have enough so that nobody else can determine your future essentially.”

I would add to this that people don’t think about the “one in a hundred-year” storm enough. I’d like to think I can run this business for 40 years – which means there’s a pretty good chance we’ll come across one at some point. We need to be sure that both your investment and the business will survive it.

Some time ago I read an article on Warren Buffett and cash. His view was that the real reason you hold cash was that it was an open ended option (that did not decrease in value) which gave you the right to purchase shares when opportunities presented themselves. In other words cash allows you to be an opportunist.

How does this compare to the Australian Fund? Would there be any chance of seeing a similar graph for that fund?

The Australian Shares Fund holds many illiquid investments. We would not be able to sell our investments quickly without forcing prices down. So we tend to own a higher cash balance in that fund.

Nice post Alvise, some good points.

But that last sentence…how do you say ‘straw man’ in Italian? None of us in the pro-cash camp are arguing for permanently sitting on a huge pile of cash. We’d instead argue that an oscillating cash balance is a better strategy than a permanently invested one. Especially when some of the cheap stocks you might choose to sell (to buy cheaper ones) are illiquid normally, and likely to be even more illiquid in times of general market duress. And psychologically, selling cheap is easier in theory than in practice.

I like the Peter Lynch approach and if the opportunities are present then we might as well get caught with our pants up. The flexibility the fund has around what it can invest in, cash levels, weightings and listed / unlisted assets combined with its investors attitudes are its greatest advantage. So when you need to break convention, go for it because many others cant.

I’d prefer my fund manager be at or near fully invested. If I want to hold more cash I can do that myself outside the fund.

Agree. And I won’t have to pay a management fee for the cash held outside the fund.

I’m an 80:20 man myself

I’ve always disliked selling cheap to buy cheaper, as it normally entails crystalising losses and per Gareth’s comments, is never fun with illiquid securities. That being said, the recent sell off in the US and the lack of funds I had available to take advantage meant I had to do that for the first time, so far so good.

Isn’t cash really just a product of the portfolio? As positions reach close to our assumed value, they’re trimmed and in the absence of new ideas, we accumulate cash. When ideas are abound, the cash position reduces. Presumably you also need a buffer for withdrawals, but hopefully it’s tiny given most of us are here for the long haul.

If we have another 10% selloff and you’re unable to take advantage, as long as you aren’t afraid to ask for new inflows (just like last year), I’m comfortable with a skinnier cash position than I might have in my own personal portfolio.

fortune favours the bold…

now is the very time for Fora-gerians to park cash into FISF with unit price down 10% since August 2015

FISF $80m and 1,334 investors

invest $5,000 each and FISF will have an additional 8.3% cash

if August 2015 was the time,

then February 2016, 3 year anniversary is definitely another time to celebrate collectively with a buy in

Easy to say, but not all of us have the $5,000 lying around. That’s why we drip feed an amount every month.

My view (I’m a former fund manager), is that the “dry powder” argument only applies when your FUM is above a certain threshold, relative to the size of your investable universe and the level of fear/greed that is prevalent in the market at the time.

Broadly speaking, my rule of thumb is that if you manage less than 1/200,000th of the total capitalisation of a market, then the opportunities to be 100% invested, 100% of the time are out there. Accordingly, the only reason for not being fully invested is if one doesn’t have the time, ability or inclination to do the enormous amount of digging required to find the right opportunities.

There is some reasoning and research behind this figure, but I’ll leave that out for now.

On the ASX this translates to about $8m, which is peanuts at the institutional level, but is more than most individuals or SMSFs will ever get to invest on the ASX.

Obviously, this figure needs to be adjusted to reflect prevailing market conditions, specifically, it is based on the prevalence of quantifiably bargain priced stocks at the 2007 peak, right now it should be quite a bit higher.

The family SMSF that I manage was fully invested at the 2007 peak (it was less than $8 at the time), and despite taking enormous losses on some of the securities that went bust over that time, we’re still sitting on double digit per annum returns from that peak, despite the fact that the broader market is down and the consensus view is that 2007 was an awful time to be invested.

People also seem to forget that there are no null choices in asset allocation/management. Wealth is merely the expression of the productive capacity or ownership interest to which an investor is entitled. This can be expressed as ownership of a business, real estate, yellow metal, institutionalised promises, or even pieces of computer data that can be exchanged for just about anything because everyone on the planet believes that they are valuable.

The idea that an investor can avoid risk or even maximise his long-term opportunities by keeping a portion of his wealth in cash at all times, seems a little tenuous. But even if it were true, there are other ways of achieving similar outcomes without the need for so much cash.