Share

Share  Download

Download Following the collapse of Dick Smith (DSH), and the poor performance of floats like Myer (MYR) and Spotless Services (SPO), the public offerings market and the role of private equity is under scrutiny like never before.

While everyone is bashing private equity, not every PE float is a bad one. Indeed, if you had bought both Dick Smith and fellow 2013 private equity float Veda in equal proportions, you would have generated a healthy overall profit despite Dick Smith going to zero (Veda was taken over in late 2015 at a 126% premium to the float price).

So how you can you distinguish between the two? Here’s a quick guide to steering away from the next lemon.

1) Consider who the seller is and why they are selling now

Don’t be lulled into thinking that floats are an easy way to make low risk money. You are actually at a very real disadvantage; the seller knows an awful lot more about the business than you, and they are keen to be on the other side of this transaction.

At the very least you must consider who the seller is and why they are so keen to sell now. If the future of the company is so great, why head for the exits? If the seller is private equity, you know they have done this many times and know how to turn a profit. How much of the business are they selling (the less the better)? And how long have they held it for?

PEP, the private equity company behind the Veda listing, had owned the company since 2007. Many private equity mandates require an exit within a specified time frame, so they may have been forced to list it.

Contrast that with Dick Smith. There’s only one reason you would list a company having only owned it for nine months, and that’s because you think the timing is ideal.

2) You are reading a completely biased document

Brochures for holidays are designed to encourage you to buy, and so are brochures for floats. Don’t be fooled by the official sounding title prospectus, it’s not written by some sort of independent umpire. Despite ASIC’s best efforts, this is a sales piece written by the seller to help sell shares at the best price possible.

You are reading an utterly biased document. Expect the good parts of the business to be overly emphasised, and the challenges and threats to be glossed over. Don’t just accept what you are told. Put your sceptical hat on and ask hard questions when reading.

3) What’s missing?

Following right on from the previous point, don’t be fooled by the apparent level of detail. A prospectus can be 200 pages long but be missing a lot of the most important information (as a general rule, the most important stuff will be in the smallest font in the document). A good way to detect what’s missing is to ask ‘what do I need to know about this business’ before you even start. Make a list, then go and read the prospectus. Whatever is missing will stand out like a sore thumb.

Wherever management don’t dwell, that’s where you want to focus your attention. Why do they only show you 3 years revenue history when they could have shown you 10? Have a look at this chart from the Veda prospectus, showing historical revenue going back 20 years:

Why don’t we have anything like this in the Dick Smith prospectus? The answer is obvious.

When the seller has the choice as to what they include in the document, what they don’t tell you is more important than what they do.

4) Any one year’s profit is unimportant

I should caveat this by saying one year’s bad profit result can be important and should be looked at closely. That aside, an easy way to get duped it to place too much reliance on one year’s profit, whether it’s last year’s or next year’s forecast.

Even when signed by an auditor, no profit number is gospel. As anyone who runs a small business can attest, there is a lot of discretion as to what profit is reported each year. This can be done through a range of accounting means, such as taking provisions in prior years that benefit future profits, or adjusting depreciation charges, but also by a range of physical means. Has the company simply squeezed expenditure in an unsustainable way to prop up profits? Or spent a lot of money in June last year so it didn’t have to be spent this year?

Even if the profit were reliable, you still shouldn’t place much weight on it. If you pay $3 for a company, and next year it earns $0.20 per share rather than the $0.15 per share forecast, that’s only worth 5 cents to you. The increase is less than 2% what you’ve paid for the shares, unless the extra earnings have real, ongoing predictive power.

If you’ve paid 15 times earnings in a float, the business needs to be making good profits for decades ahead. Many newly floated companies achieve their forecast in early years and come unstuck later. Focus on the long-term potential of the business not next year’s profit.

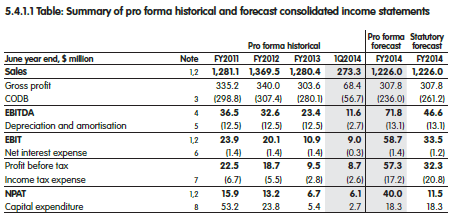

Let’s take a look at what we were actually given with Dick Smith:

According the “pro forma” numbers, it made $22m in 2011, $19m in 2012 and $9m in 2013. Those numbers don’t include 73 presumably lossmaking stores that were closed during that period, and profits have been increased to reflect lower depreciation expense thanks to “fair value adjustments recorded to plant and equipment”. Are you sure you want to pay $520m for that business?

The one number used to justify the float price was a $40m pro forma forecast for 2014. That’s a lot of emphasis on one year’s hypothetical profit.

5) Be wary of trends

Research by psychologists like Daniel Kahneman shows that human beings are very poorly wired for investing. Chief among our shortcomings is a shocking tendency to mindlessly extrapolate anything that looks like a trend.

Imagine if I had a company that produced these profits in the past 3 years:

Looks like a real loser right? After all, profit keeps falling. How much would you pay for this? Maybe $50m? But remembering how easy it is to shift profits around, what if I took a $2m provision in year 1 and then used it in year 3? For most businesses that’s easy to do in a range of legitimate ways. Then profits would look like this.

Looking at that trend, our mind naturally imagines profits growing into the future. How much would you pay for that business? Fifteen times earnings or $150m might sound fair? The point, of course, is that the seller knows what you want to see, and they will do their best to give it to you. And it’s very easy for them to create a trend. So be wary.

Conclusion

Remember also that no one ever forces you to buy shares in a float. There are plenty of other things, and probably better things, to invest in. As Warren Buffett puts it:

It’s almost a mathematical impossibility to imagine that, out of the thousands of things for sale on a given day, the most attractively priced is the one being sold by a knowledgeable seller (company insiders) to a less-knowledgeable buyer (investors).

If you do wish to invest in a float, pay close attention to who the seller is and what their motivations are. Most likely their goals aren’t consistent with yours.

Then go one step further, and consider that the seller has also thought about you and your motivations, and is trying to show you exactly what they think you want to see. Every bit of communication you get is going to have this taint to it.

As the saying goes, buyer beware.

Want to know more about the style of investing we practice at Forager? Check out our page what is value investing

Thanks Matt

A very concise and spot on article. Surely ASIC must be more pro active and demand better financial information before approving the contents of a prospectus. If they are the “watch dog’ then they are not very effective at present.

Thanks for your thoughts Michael. Almost all disclosure documents contain these words ‘neither ASIC not ASX takes any responsibility for the contents of the Prospectus or the merits of the investment to which this Prospectus relates. My two cents: treat those words seriously. There’s probably a few things that can be done to improve disclosure, but it’s not the regulators job to stop people from participating in an overpriced float. No regulator could ever do that.

It’s unreasonable to be asking ASIC to review all prospectuses at the time they are lodged (i.e. – be proactive). It would expensive to permanently staff an office with people who likely wouldn’t be 100% utilised at all times and some might see a ‘no issues’ mark from ASIC as a tick of approval that the listing company is a good investment. There could also be issues with the prospectus that aren’t immediately apparent – and a subsequent prosecution could be jeopardised by a previous ‘no issues’ assessment by ASIC.

The current system leaves the issuer of securities (and their professional advisors) open to civil penalties (i.e. compensation of investors) for misleading statements or omissions of relevant material from a prospectus. Surely the most important asset these professional advisors have is there reputation in the market – they wouldn’t be trashing that for a one-off engagement fee.

If people want to see improvements in prospectus disclosures they should read the relevant ASIC regulatory guidance (RG 228 – Effective disclosure for retail investors) and lobby government and ASIC for changes. The necessary financial disclosures section in RG 228 to my mind is too earnings focused and little attention is given to cash flows and the historical working capital position of a business (the latter a key consideration in private trade sale financial due diligence engagements). Read the DSH prospectus and you’ll find negligible information on these matters. If such disclosures were mandated the obvious inventory liquidation undertaken by Anchorage in FY13 would have been immediately apparent.

However no regulation can stop people from buying shares in a company that has been priced on an earnings figure that the business is yet to achieve (and paying top dollar without obtaining a margin of safety for the inherent execution risks in achieving those forecast earnings).

Pingback: 5 tips to help you avoid investing in the next Dick Smith | Business Insider

Great article Matt. I think the big area that we possibly take for granted, and this Dick Smith IPO shows up pretty clearly, is that there is a fundamental conflict of interest with almost all the professionals and advisers involved. The Investment Banks, the Accountants, the Lawyers, even some analysts.

Perhaps indicative of the changing face of professions whereby the business/profit motive overrides the service/social obligation. The retail investor assumes the latter while those dealing with this sort of thing all the time favour the former. In other words we expect more from the professionals in these IPO’s in much like a gatekeeper role rather than being conflicted by having their finger in the pie as well. It must colour their opinions and reports.

I am concerned that we see litigation as a solution to false and misleading statements. We have fair trade offices for $20 toasters but we expect people to police the statements in a prospectus. I cannot accept that the professionals have the risk of reputation – these are constantly recreating themselves under new banners. The attorneys cannot be held responsible for the facts and the sponsoring broker and other parties are all earning fees and that is a primary motive. I think that there should be a fee paid to ASIC to lodge a prospectus and part of your listing fee should cover ASIC surveillance. Often by the time you call an end to the company there isn’t enough money left in it to recover anything and pursuing the directors can be very expensive , often made more so as the company paid for a policy to defend them. There has to be something better than we have. Managed investment schemes had a lot of people earning fees , commission etc and then when the timber ones failed many said it was a rort. No-one thought that the maintenance fees should have been put into a trust and only released each year over the period for which they were paid upfront. Given the weighting to exploration on the ASX I think many just don’t see investing as viable for the average person. I think that we can all name a few investments that really by the time they folded we would have loved to have the resources to investigate. I didn’t hold DSH – I would love to think by skill but on others at times I think I may have been lucky. In reality I can even name a company where the director had to be pursued for very large amounts he spent on his private boat – ASIC nowhere to be seen.

ASIC did question disclosure but let it through in the end. The issue here is the DDC. Both the IAR (Deloitte) and JLMs (Maq and GS) have a lot of questions to ask. Finally the company directors sign off on the document so really they have some questions to answer. Finally investors should do more work before buying a stock.

My view on one to watch – Bellamy’s. No supply, no manufacturing no approved china licence yet $1.3b market cap. $300 to $500m at best.