Share

Share  Download

Download Last week I was researching the stock of a multibillion dollar company for the Forager International Shares Fund when Chris, our bright young analyst asked – what sort of edge do we have here? What insight can we have that the market doesn’t?

He had a point. Aren’t we supposed to be ‘the smartest guys in an empty room’? Shouldn’t we limit ourselves to smaller, obscure companies where we can maximise our nimble size and research advantages?

After all, the majority of our most successful investments such as B&C Speakers (BIT:BEC), Kapsch TrafficCom (WBAG:KTCG) and Lotto24 (DB:LO24) came about because of our willingness to look where others weren’t or couldn’t.

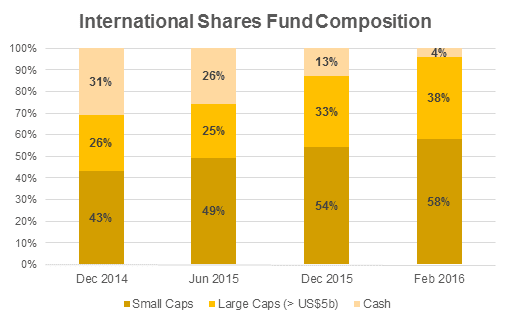

As you can see from the chart below, the core of the portfolio is still invested in ‘small caps’ and we have added new investments in such stocks. You can also see that we have invested more in ‘large caps’ too.

‘Large caps’? Isn’t that the most crowded room of all?

Well, the share prices of these large and deeply-researched firms can also be weighed down from time to time to levels well below their intrinsic value by general market pessimism.

Most notably, during periods of excess fear even companies with rock-solid balance sheets and wide economic moats have their share prices tarnished. In such situations, many investors tend to sell first and ask questions later. Other market participants trade on momentum. Look no further than the global financial crisis of 2009.

As explained in ‘The Baupost Investing Way’, during such periods when ‘the tide goes out’, ‘suddenly, the market shifts violently and a handful of stocks [irrespectively of their size] immediately offer a compelling margin of safety’.

Apart from times of general pessimism, large companies can run into problems and suddenly become unloved.

Often these problems can be fixed over two or three years, but Wall Street’s focus on the next quarter or the next year means that the stocks of even the most impressive corporations can be dumped pretty quickly. Sometimes too quickly, providing opportunities for value hunters.

Our focus remains on smaller, under-researched companies. But thanks to increased concerns about the Chinese economy, tumbling commodity prices and some company-specific bad news, we have been able to invest in a number of high quality large caps at attractive prices in recent months.

At Forager, we’ll go where the returns are.

Hi Alvise,

I’m happy for the fund to have a ‘small-caps’ angle to investing but I’m glad you’re not dogmatic about investing solely in one size-segment of the market. Please, by all means, buy large caps when there’s value, and I’ll look forward to redeeming our investment sometime around 2040. Yes, we’re patient investors.

Keep up the good work.

Ed

Don’t forget perspective. A Multi billion dollar market cap will barely get you in the S&P 500. Sub 1billion is small fry in the US.

Thanks Alvise.

Your post goes some way to addressing issues flagged in my email of 3 Feb regarding investor communications and FF relative strengths as a funds manager and approach to identifying prospective investments. You might like to follow that up…

Ta, Ron